ECONOMIC FORECAST

California Economy on a Sound Footing for the Next Two Years

More young people are moving out of their parents’ homes, unemployment is inching downward, and gasoline prices are among the lowest in years.

All signs point to the U.S. and California economy picking up speed in 2015 and 2016 and leaving the Great Recession in the dust.

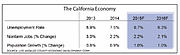

The U.S. gross domestic product is expected to rise 3 percent this year and next compared with 2.4 percent growth seen in 2014.

Nationally, unemployment should remain around 5.6 percent this year and drop to 5.4 percent in 2016 while California’s unemployment rate will shrink from its current 7 percent to 6.7 percent later this year and 6.3 percent in 2016.

That was the forecast predicted by the Los Angeles County Economic Development Corp., which released its “2015–2016 Economic Forecast & Industry Outlook” on Feb. 18.

The good news is that California’s economy is expected to grow even faster than the nation as the housing industry builds up new inventory, more people find jobs, and the millennial generation starts to move out of Mom and Dad’s basement into an apartment or house.

“The real key to 2015 and 2016 is the situation with real estate,” said Robert Kleinhenz, the LAEDC’s chief economist. “At some point, we expect to see millennials [those born in the early 1980s to the early 2000s] come into the housing market, which will put pressure on apartment occupancy and single-family homes. This will unleash construction activity, which is somewhat overdue in California and long overdue on the national level.”

Demand for new and old homes will be bolstered by another demographic that was devastated by the recession: those people who lost their homes through foreclosure or bank repos. It takes seven years to come back from personal bankruptcy and a foreclosure. Many have repaired their credit-worthiness and are ready to replace the homes they lost.

Construction employment in the state is predicted to shoot up 5.6 percent this year and 6.3 percent in 2016 after growing 5.6 percent last year, when 35,700 construction jobs were added. However, these gains still won’t offset the 373,900 jobs lost during the recession. At its peak, the construction industry employed 933,700 in 2006 before dropping to a low of 559,800 in 2010. Last year, 672,000 people in California were employed in construction.

Already, shortages of skilled workers—such as equipment operators, carpenters, project managers and supervisors—are being reported.

Other strong job growth areas will be in the healthcare industry. Last year, healthcare added the most jobs in California, with an uptick of 67,900 workers. “Health services is a safe bet for job growth because it saw job gains even during the recession,” Kleinhenz said. “With the aging population and increased access to healthcare because of the Affordable Care Act, it points to growth in that industry.”

Growth was also robust in the administrative support and waste-services industries, which added 48,500 workers last year, followed by leisure and hospitality with 46,000.

International trade—which centers around the Port of Los Angeles, the Port of Long Beach and Los Angeles International Airport—will rise nicely if the seaports can resolve their congestion problems. “International trade has great potential in 2015,” Kleinhenz said “Imports should pick up pretty good in 2015 with the economy growing while exports should be flat or up a little bit because of the strong dollar.”

Dialing for oil dollars

Economists had expected to see a rash of consumer spending after gasoline prices plummeted from around $4 a gallon last year to about $2.75, but that hasn’t been the case. Nationally, retail sales in January dipped 0.8 percent. “We still have a cautious consumer out there,” Kleinhenz said, noting that many people don’t realize that gas prices will remain fairly low until the end of the decade.

Consumers affected by the recession are taking their gas savings and paying off credit card debt accumulated from the holidays or earlier. Many people still are not earning as much as before the recession.

When adjusted for inflation, the median household income in the United States is 10 percent lower than in 1999, when it was $56,900. In 2013, it was $51,900.

“At some point, we should see some of the savings from lower gasoline prices show up in retail sales for clothing and other types of goods,” Kleinhenz said. “But it may take a while for that to show up.”